Amid heightened geopolitical tensions in the Middle East, Latin America has experienced a sharp reversal from being the top-performing region within Emerging Markets in 1Q26 to a relative underperformer in 2Q26. The resulting rise in energy prices altered expectations for the global interest-rate cycle and weighed disproportionately on Latin American markets, which have some of the world’s highest real interest rates. In addition, the region had limited participation in the narrow, AI-driven rally that dominated returns year-to-date. As the US progresses towards conflict resolution with Iran, many variables that acted as headwinds are likely to become tailwinds. Latin America offers an appealing set of bottom-up opportunities, while the broader region presents attractive valuations, scope for monetary easing, and light investor positioning. Against this backdrop, we believe Latin America is in the right place, at the right time.

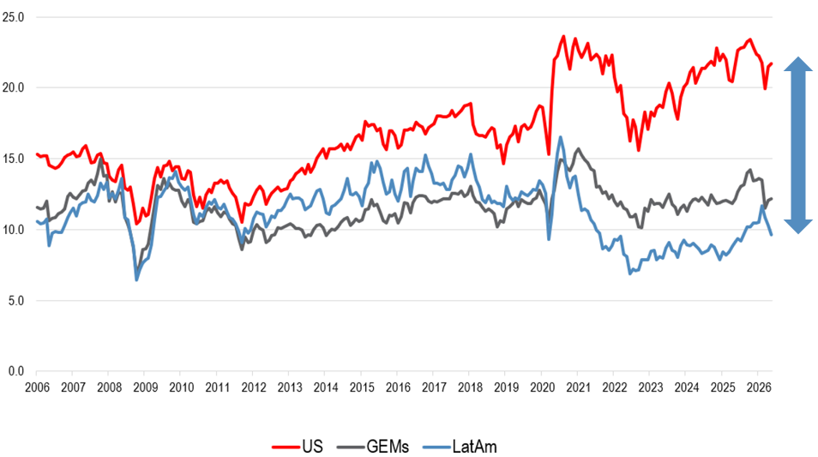

Latin America remains the world’s most inexpensive region, trading at 9.6x forward P/E. Valuations are below their own historical average and at a major discount to U.S. equities. In an environment where U.S. equity valuations are approaching near historic highs, partially driven by Technology sector multiples, Latin America offers a valuable diversification benefit. MSCI Latin America’s Technology weight is less than 1% whereas MSCI Asia’s Technology weight is nearly 54%.

MSCI Latin America Fwd. P/E at a 50% Discount to the U.S.

Source: J.P. Morgan, Bloomberg Finance L.P., MSCI

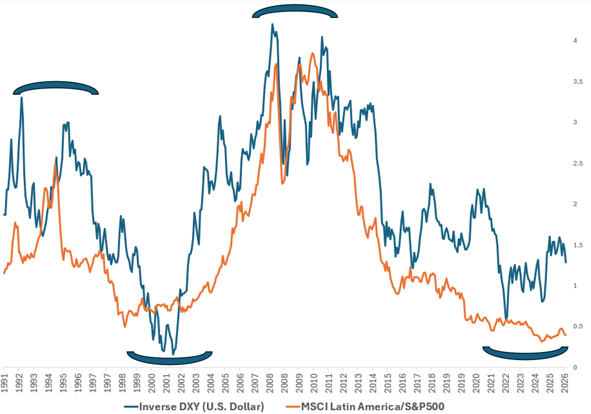

Latin America directly benefits from the rotation out of the U.S. dollar. The region has some of the world’s highest foreign exchange carry as the U.S. dollar weakens. With the backdrop of the U.S. and Eurozone deficits expanding and in a scenario of a weak U.S. dollar, Latin America stands to gain through improved management of external financing needs, favorable commodity pricing, and stronger trade competitiveness. Historically, this has been supportive from an equity perspective, with Latin America’s outperformance relative to U.S. equities often coinciding with periods of U.S. dollar weakness.

MSCI Latin America Performance vs. S&P 500 and Inverse U.S. Dollar

Source: Bloomberg Finance L.P.

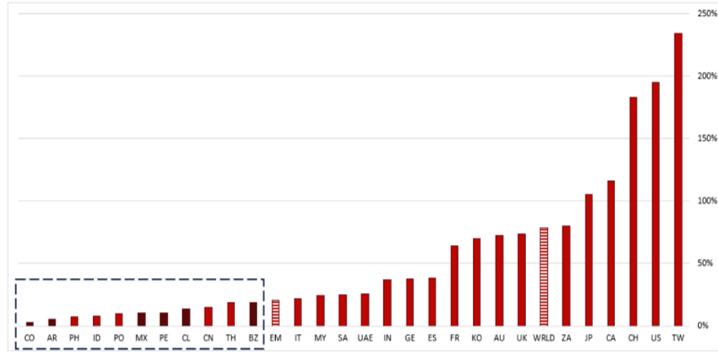

Investor positioning remains light. Perhaps surprisingly, Latin America only represents 6.4% of the MSCI EM Index weight. For context, 20 years ago it represented 19.9% of the Index which coincided with a weaker U.S. dollar and strong commodity demand, driven by China’s industrialization. This time around it should be driven by strong demand in select commodities, energy security and AI infrastructure. Additionally, Latin America has decisively moved to the center politically, with Argentina, Chile, Peru, Colombia, Honduras, El Salvador, and Bolivia all governed by centrist governments. Lower interest rates could trigger domestic portfolio inflows to Latin American equities which would increase the overall equity allocation of local savings from a historical low of 6% to 15% by 2035, as per Morgan Stanley. In our view, a little effort can go a long way.

Stock Market Capitalization/GDP – Latin America Is More Sensitive to Rotation

Source: MSCI, IMF, Bradesco BBI

Mexico

Mexico remains one of the primary beneficiaries of the global nearshoring trend. Despite common misperceptions in the news surrounding tariffs and benign GDP growth of 1.2% expected for 2026, foreign direct investment reached a record USD 23.6 billion in the first quarter of 2026, representing growth of 10.4% year-over-year.

Within this context, we see Ternium as a differentiated opportunity. Ternium is a leading flat steel producer with operations spanning Mexico, Brazil, Argentina, and the United States. Following a period of elevated capital investment, Ternium is beginning to ramp production at its state-of-the-art Pesquería facility in Mexico. The ramp-up progression has exceeded expectations thus far, with utilization expected to approach full capacity by late 2026. The facility will increasingly integrate steel production that was previously sourced internationally, improving Ternium’s efficiency and positioning in serving higher-value end markets. USMCA negotiations remain a key variable. Current steel price differentials between Mexico and the United States remain elevated due to tariff uncertainty from the reinstatement of Section 232 tariffs of 25%, which was later escalated to 50% in June 2025. This is particularly striking, given that the U.S. is a net exporter of steel to Mexico. Looking ahead, any reduction in trade barriers could improve industry economics in Mexico.

DRZ PM Marc Miller (Middle) at Ternium’s Pesquería Production Site in Mexico

As the nearshoring trend continues, Vesta should be one of the main beneficiaries of the shifting global supply chains towards Mexico. Vesta is a leading industrial real estate development company, which has one of the largest and most modern property portfolios in Mexico. Over recent years, Vesta has expanded its land bank reserves meaningfully in core markets such as Guadalajara, Monterrey, and Mexico City. As they continue to develop projects in these areas, the company should be amongst the best-positioned players to capture the demand across key nearshoring corridors. We believe supply chains will continue to relocate to Mexico due to the proximity to the U.S. Cost competitiveness also remains the driver at the forefront for many corporations expanding into Mexico. Despite several minimum wage increases over recent years, the average manufacturing wage in Mexico is $5.00/h, which is below China at $6.50/h average, as per North American Production Sharing (NAPS), and the U.S. above $30/h, as per MSCI. Furthermore, Mexico also has a young and increasingly skillful workforce. The U.S., in contrast, has 80% of the jobs in the services sector, and a shift back to labor-intensive parts of the supply chain would likely be harder to achieve, making Mexico the obvious choice as the next manufacturing hub. On July 1st, the USMCA (United States-Canada-Mexico Agreement) renewal was not agreed upon, and there is the third round of bilateral talks scheduled for July 20th. While we expect some volatility regarding the timing of the USMCA renegotiation, we believe ultimately some form of renewal should prevail due to Mexico’s strategic importance to the U.S.

DRZ PM Marc Miller (Right) in Mexico With the CEO of Vesta

Peru

The outcome of the recent elections with the victory of a more moderate candidate, Keiko Fujimori, presents a once-in-a-generation opportunity for the country. Peru has had nine different presidents, coupled with social unrest, which has weighed on economic momentum in recent years. Nonetheless, Peru outperformed many regional peers, with GDP growth exceeding 3% in each of the past two years. Looking ahead with the new government, Peru has the potential to unlock higher foreign direct investment and accelerate long-delayed infrastructure projects, including road networks and airport modernization. Management teams across leading Peruvian corporates have highlighted the potential for GDP growth to reaccelerate under the new administration, translating to higher loan growth, with mining expected to remain a key driver of investment. Furthermore, this election cycle also marks the return to a bicameral legislature following reforms approved in 2024. Congress’ composition has already been determined, creating an improved institutional check on the government.

Against this backdrop, Credicorp remains one of the most attractive financial franchises in the region. As Peru’s leading financial services company, Credicorp combines a dominant banking franchise BCP (Banco de Crédito del Perú), with ownership of Yape, the country’s leading super app.

Currently, 82% of the economically active population in Peru utilizes Yape. But the data point itself does not tell the full story. Yape is not just an app in the eyes of the Peruvians, but rather a community – as most Yape users refer to themselves as “Yaperos”. Yaperos use Yape in most everyday payment transactions. We see room for Credicorp to further leverage Yape’s footprint, given that Yape is now evolving its strategy from transaction frequency to monetization, predominantly through lending. This is significant, given that Peru is one of Latin America’s more underpenetrated markets, with loans representing only 35% of GDP, cashless payments well below regional countries, and about 7 million micro-entrepreneurs with no access to formal credit, as per the OECD. Yape is well positioned to capture this opportunity, offering loans to a segment of the population that did not have access to credit before. Management expects the portfolio to expand meaningfully over the next few years as customers migrate toward larger and longer-duration lending products, and drive Yape to become the second largest profit-contributing business of Credicorp. Despite new market entrants such as Revolut. Yape’s dominance should continue to be supported by its strong brand recognition. Beyond Peru, additional opportunities exist through Yape’s expansion into Bolivia, a market that underwent a shift toward a more market-friendly government last year.

DRZ PM Marc Miller (Left) in Peru With the CEO of BCP (Banco de Crédito del Peru)

Brazil

Following a more centrist wave in recent election cycles across Latin America, Brazil stands out as one of the few major markets where the political cycle has yet to turn. After years of populist policymaking and some of the world’s highest real interest rates, the scope for policy normalization remains significant.

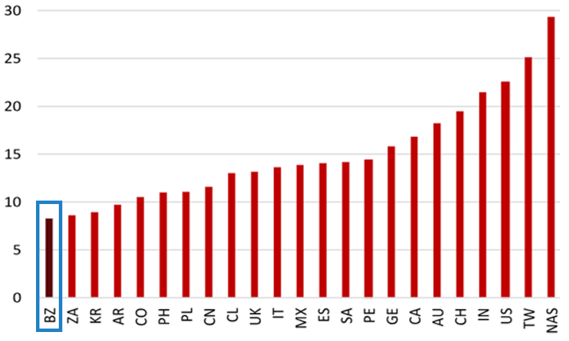

An easing monetary cycle coinciding with a presidential election in October would be a combination not seen since 2006, potentially creating a more constructive backdrop for Brazilian equities. Current polls favor the incumbent President Lula, a scenario we believe is already reflected in valuations. The Ibovespa Index trades only at 8x forward P/E, making it one of the most inexpensive equity markets globally. President Lula’s re-election would likely imply policy continuity, which should not meaningfully change the bottom-up fundamentals for Brazil.

Brazil Is the Most Inexpensive Major Equity Market (12-Month Forward P/E)

Source: Bradesco BBI

We believe BTG Pactual is particularly well-positioned. As one of Brazil’s leading financial institutions, we believe BTG should continue gaining market share across its diverse businesses while expanding its presence throughout Latin America. Under the leadership of Chairman André Esteves, who co-founded the company, the firm has had a complete transformation, strengthened its competitive positioning, and scaled profitability. Since 2018, BTG has more than doubled its market share in several segments, such as investment banking, asset management, and retail banking, while it has been scaling further into private payrolls.

A scenario of a faster rate-cutting cycle would likely create a more supportive backdrop for capital markets activity, increase participation from local equity investors, and stimulate corporate investment, all of which would benefit several of BTG’s core businesses. We also believe the market underappreciates the extent of BTG’s transformation. Today, the business model is more asset-light, with asset and wealth management divisions contributing to a larger share of earnings. As a result, we see potential for a more fundamental valuation re-rating. Conversely, if rates were to remain higher for longer, BTG should continue to leverage its fixed-income franchise and lending divisions. A case in point would be the company’s performance in recent years, marked by high interest rates, where BTG expanded its adjusted return on average equity from 20.3% in 2021 to 26.9% in 2025.

DRZ — Our Differentiating Factors

To conclude, we believe Latin America is on the cusp of a multi-year re-rating story, and the recent underperformance offers an exciting opportunity to revisit the investment case. We are guided by our 30+ year investment process and deep local knowledge of the region, which supports our fundamental bottom-up investment approach.